What is Budget?

It is the process of preparing and overseeing a financial document that estimates income and expenses for a period. For business owners, executives, and managers, It is a key skill for ensuring organizations and teams have the resources to execute initiatives and reach goals. In other words, the approved cost estimate for the project any work breakdown structure components, or any schedule activity.

Generally, the word budget is concerned with the limitation on spending. For example, the government approves spending for their various bodies. Then they expect the bodies to keep their expenditures within the limit prescribed by the budget. In contrast, many business organizations use to focus alternation on company operations and finances. Not just to limit spending, budgets highlight potential problems and advantages early, allowing managers to take steps to avoid these problems or use the advantages wisely.

A budget is a tool that helps managers in planning and control functions. Interestingly, it helps by using a control function not only looking forward but also looking backward. It, of course, deals with what manager’s for the future. However, it can also be used to evaluate what happened in the past. It is a benchmark that allows managers to compare actual performance with estimated or desired performance.

R.H Garrison states, ” A budget is a detailed plan outlining the acquisition and use of financial and other resources over some given period. It represents the plan for the future expressed in formal quantities terms. The act of preparing a budget is called budgeting. The use of budget to control a firm’s activities is known as budgetary control.”

According to the Chartered Institute of Management Accountants, London, “A financial statement or a quantitative statement prepared and approved prior to a defined period of time of the policy to be purposed during that period for the purpose of attaining a given objective.”

Thus, It refers to ‘accounting for the future’. it summarizes the estimated result of future transactions for the entire company in much the same manner as the accounting process records and summarizes the result of completed transactions.

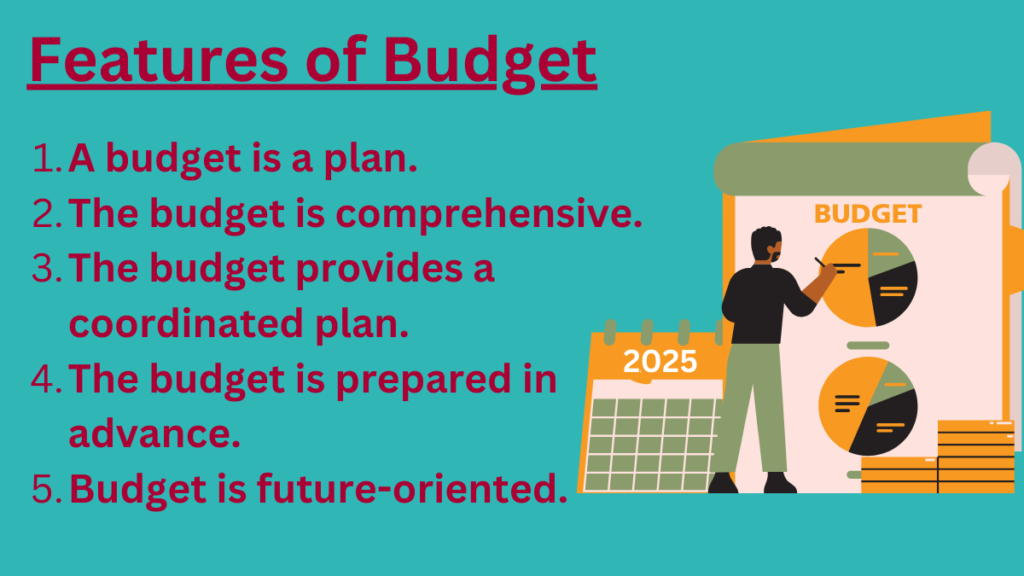

Features of Budget

Budget is a plan:

it is an expression of the plan for the operation of an enterprise. The operations of an enterprise are affected by some factors both external (such as general business conditions, government policy, and size as well as the composition of the population) and internal (such as manufacturing processors, promotional programs, etc.). It covers both external and internal factors and expresses partly, what the management expects to happen and partly what the management intends to happen.

It is comprehensive:

It is comprehensive which means that it covers the activities and operations of all the segments or decisions of an organization. It is prepared for each segment or division of an organization and all these are integrated into the master budget.

It provides a coordinated plan:

It is prepared for the variable segments or divisions of the organization after considering the conditions and problems of each segment. It helps to coordinate among the sections and departments of an organization.

It is prepared in advance:

It is prepared in advance and includes future courses of action. thus, a budget is forward-looking in in approach.

It is future-oriented:

It always relates to a specified future period. It becomes meaningless if it is not related to a time horizon. Thus, production, sales, profit, etc. are planned to be achieved in a pre-determined time.

Importance/Functions/Objectives of Preparing Budget

- To plan the policy of a business for the next period for the achievement of the firm’s objectives and its translation into monetary and quantitative terms.

- To determine the responsibility of each department and executive so that they are made accountable for definite and precise results.

- To coordinate the activities of a business so that each is a part of an integral total.

- To provide for continuous comparison of actual and performance in terms of results achieved and cost incurred so that the cause of any inefficiency is immediately detected and removed.

- To control and direct each function so that the best possible results may be obtained.

- To provide for the revision for the future in the light of experience gained.

Advantages & Disadvantages of Budgeting

Advantages:

a) Improved planning and control

You can plan and identify potential financial issues before they arise. By setting targets and monitoring performance, you can make informed decisions that will help you achieve your goals.

b) Better resource allocation

It helps you allocate resources effectively and avoid overspending. This can help you maximize profits and reduce waste.

c) Enhanced communication and coordination

It can help you communicate financial goals to your team and ensure that everyone is on the same page. It can also encourage teamwork and collaboration as your staff work together to achieve common financial targets.

d) Increased motivation

When your staff knows that there are financial targets to meet, they may be more motivated to work harder and achieve better results.

e) Facilitates decision-making

With a budget in place, you can make informed decisions about financial matters, such as whether to invest in new equipment or hire additional staff.

f) Increases profitability

By managing financial resources effectively, a budget can help increase profitability and improve overall financial performance.

Disadvantages:

a) Inflexibility

It can be inflexible and may not allow for unexpected changes in circumstances. This can lead to missed opportunities or inefficient resource allocation.

b)Time-consuming

Creating and monitoring can be time-consuming and may take away from other important tasks.

c)Potential for conflict

It can create competition among staff and departments. This can lead to conflict and may not be conducive to teamwork and collaboration.

d)Unrealistic targets

If targets are set too high, it can create undue stress and may lead to burnout among staff. It’s important to set realistic targets that can be achieved with the available resources.

e)Can be too complex

It can become too complex and difficult to understand, which may make it less effective as a management tool.

f)May not reflect reality

It may not always reflect the actual financial performance of a hotel, especially if it’s based on unrealistic assumptions.

Types of budget

Manufacturing Concern:

a) Sales budget

It is the starting point in preparing the master budget. It is a detailed schedule of expected sales for the coming period. It is usually expressed in both amounts and units. Once the sales budget has been set, a decision can be made on the level of production that will be needed to support sales and the production budget can be set well. It is constructed by multiplying the expected sales units by the sales price. Generally, It is accompanied by a computation of expected cash receipts for the forthcoming budget period. It is needed to assist in preparing the cash budget for the year.

b) Production

It is prepared after preparing the sales budget. This is an estimation of the quantity of goods to be manufactured during the period. In preparation of the production budget. the first step is to formulate policies relative to inventory levels. The next step is to determine the total quantity of each product that is to be manufactured during the period and the third step is to schedule the production for the period.

c) Material consumption

After the preparation of the production budget, a direct material or raw material consumption budget should be prepared to show the material that will be required in the production process. Sufficient raw materials will have to be available to meet production needs and to provide for the desired ending raw materials inventory. However, some quantity of material requirement will already exist in the form of a beginning raw material inventory. The remainder will have to be purchased from suppliers. It specifies the planned quantities of each raw material by time, by product, and by using responsibility.

d) Material purchase

Direct materials are required for production and must be purchased and each period in sufficient quantities to meet production needs and to confirm the company’s ending inventory policies. The material specifies the quantities and timing of each raw material needed, therefore a plan for material purchases must be developed. The material purchase budget is prepared based on the material consumption budget. It specifies the ending inventory of raw materials, estimated quantities to be purchased, and the estimated cost for each raw material.

e) Direct labor

f) Manufacturing overhead

g) Cost of goods manufactured

h) Administrative overhead

i) Selling and distribution overhead

j) Cost of goods sold

k) Capital expenditure

l) Cash Budget

m) Budgeted income statement

n) Budgeted balance sheet

o) cash flow statement

Trading Concern:

a) Sales budget

b) Merchandise purchase

c) Operating expenses

d) Capital expenditure

e) Cash Budget

f) income statement

g) balance sheet

h) cash flow statement